AI Loan Underwriting Implementation: Best Practices for Financial Services AI Agents

The traditional model of enterprise software procurement is obsolete. Financial institutions no longer require incremental dashboards or legacy modules; they require an accountable, outcome-driven operational workforce. AI-driven loan underwriting has matured beyond experimental pilots into a strategic necessity. When deployed correctly, AI agents do not merely assist human underwriters—they systematically eliminate manual overhead while delivering verifiable business outcomes. At Meo, we treat AI deployment as a capital-efficient workforce expansion, not a technology upgrade. By aligning agent capabilities with strict performance metrics and pay-for-performance contracting, banks eliminate upfront licensing risk and scale capacity precisely to match loan demand. This guide outlines the execution framework required to transition from fragmented automation to production-grade, audit-ready AI underwriting. It covers secure data architecture, embedded regulatory compliance, operational scaling, and cross-product workforce integration. The objective is clear: deploy an AI lending workforce that delivers measurable ROI, maintains rigorous risk controls, and operates as a seamless, accountable extension of your credit operations.

The Strategic Shift to Accountable AI in Loan Underwriting

The industry’s most frequent AI adoption failure stems from treating intelligent automation as a software feature rather than an operational workforce. Leading institutions have already transitioned from isolated proof-of-concept pilots to production-grade, outcome-driven underwriting workflows. This transition demands abandoning vague efficiency targets in favor of precise operational KPIs that track decision accuracy, cycle-time reduction, and verifiable labor cost displacement. When AI underwriting performance is measured against standardized benchmarks, it ceases to function as a cost center and operates as a profit multiplier AI Agents in Loan Processes: Best Practices.

Positioning AI agents as an accountable workforce extension fundamentally alters procurement and deployment economics. Instead of funding perpetual software licenses with uncertain returns, banks should contract agents against verified throughput and error-rate thresholds. This structure aligns vendor incentives directly with institutional performance. Modern underwriting agents operate continuously, ingesting applicant data, cross-referencing credit bureaus, and generating risk assessments without the latency introduced by manual handoffs. By establishing clear service-level agreements tied to actual business outcomes, lending executives can scale capacity on demand while maintaining strict budgetary control.

Organizational adoption requires deliberate change management. Underwriting teams must be retrained to manage exception cases, validate AI reasoning, and prioritize high-value client relationships over repetitive document verification. Positioning AI as a measurable workforce multiplier—not a replacement for institutional expertise—accelerates adoption and reduces internal friction. Accountability is engineered into the deployment architecture from day one. Every automated decision maps to a defined performance metric, ensuring capital allocation correlates directly with underwriting velocity, risk mitigation, and net revenue generation.

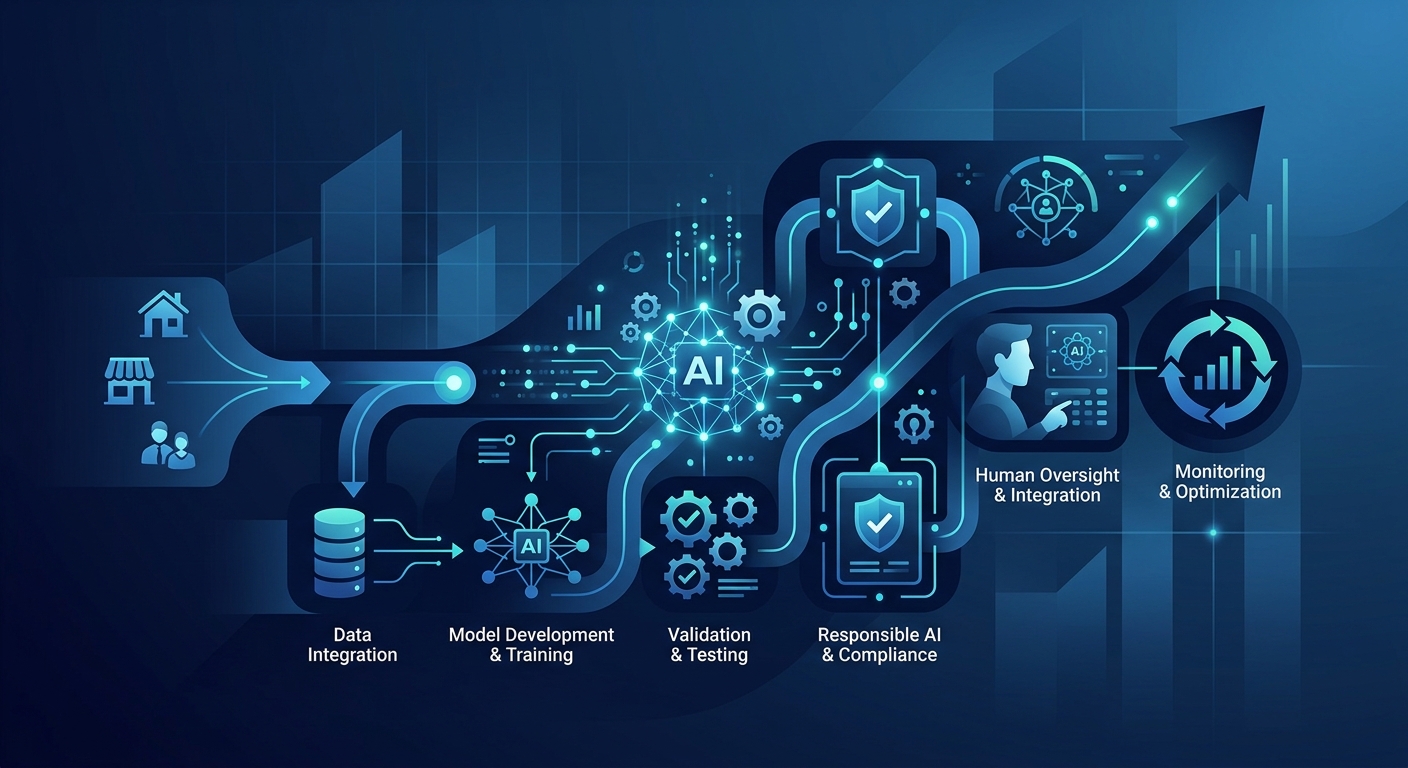

Data Integration & Secure Architecture for Core Banking Systems

Enterprise-grade AI underwriting cannot operate in data silos. The foundation of any successful deployment is a secure, low-latency API architecture that bridges legacy loan origination systems (LOS) with modern AI agents. Rather than validating documents in one platform and executing risk checks in another, an integrated AI workflow can ingest identity data, trigger AML screening, apply internal risk models, and confirm policy compliance in a single orchestrated sequence AI Agents in Finance and Banking. This architectural consolidation eliminates redundant processing and compresses decision latency from days to minutes.

Data governance dictates model reliability. Institutions must establish strict validation protocols ensuring that model training and inference execute exclusively on verified, audit-ready financial records. This requires automated data lineage tracking, real-time anomaly detection, and continuous quality scoring to prevent model drift. Regulatory mandates increasingly require explainable AI, making transparent, governed data pipelines non-negotiable for enterprise lending operations Best Practices for Integrating AI Agents in Loan Processes.

To protect existing credit risk frameworks, banks should deploy a modular architecture. By containerizing AI underwriting capabilities and routing them through secure middleware, institutions can introduce agent-driven workflows incrementally. This phased approach enables risk committees to validate performance thresholds before authorizing full production access. Modular design also ensures that AI components can be updated or replaced independently of core banking infrastructure. When integrated correctly, the AI workforce operates as a resilient overlay that enhances legacy systems without requiring costly, multi-year platform migrations. The result is a future-proof architecture that scales seamlessly with portfolio growth.

Compliance, Risk Mitigation & Audit-Ready AI Governance

In regulated financial services, innovation without compliance is a liability. AI loan underwriting must be engineered with regulatory guardrails embedded directly into the decision logic, never bolted on post-deployment. This requires institutionalizing compliance parameters for fair lending, ECOA, and BSA/AML requirements at the architecture level. When these constraints are enforced programmatically, AI agents automatically reject or flag applications that violate statutory thresholds, ensuring consistent adherence across high-volume transaction streams AI in Banking and Financial Services.

Audit readiness is equally critical. Every automated underwriting decision must generate an immutable audit trail paired with a transparent reasoning chain. Regulators and internal audit teams require deterministic explanations for credit approvals, denials, and pricing adjustments. Modern AI governance frameworks achieve this by logging input variables, weight assignments, model versions, and compliance checks in tamper-proof ledgers. This documentation standard transforms AI from an opaque risk vector into an accountable, fully inspectable decision engine.

To preserve executive oversight and risk accountability, institutions must configure strict human-in-the-loop escalation thresholds. AI agents should autonomously process standard applications while automatically routing complex, borderline, or high-value cases to senior underwriters. These escalation parameters must be calibrated against portfolio risk appetite and historical default rates. By combining automated precision with human expertise at critical decision nodes, banks maintain rigorous risk controls while achieving unprecedented processing velocity. This hybrid governance model satisfies regulatory scrutiny, mitigates algorithmic bias, and ensures accountability remains anchored in institutional leadership.

Operationalizing the Pay-for-Performance AI Workforce Model

Traditional software procurement forces banks to absorb substantial upfront capital expenditures with delayed, uncertain returns. The Meo model inverts this paradigm by operationalizing a pay-for-performance AI workforce. Instead of paying for access, institutions pay exclusively for verified underwriting throughput, accuracy, and cycle-time reduction. This outcome-based contracting structure eliminates upfront technology risk and aligns vendor compensation directly with measurable business impact. When compensation is contingent on delivery, deployment accountability becomes inherent to the partnership.

Execution requires aligning rollout phases with strict, milestone-driven business targets. Initial deployment should prioritize high-volume, low-complexity loan products to establish baseline performance metrics and build institutional trust. As accuracy thresholds are validated, the AI workforce expands into mid-market and commercial lending segments. This phased, results-validated approach ensures capital deployment scales only when ROI is mathematically verified. Executives can monitor agent performance through real-time dashboards that track processing volume, default correlation, and labor cost displacement.

The primary strategic advantage of this model is elastic scalability. Traditional lending operations require proportional hiring, training, and overhead expansion to manage volume surges. A pay-for-performance AI workforce scales dynamically, absorbing seasonal spikes or market-driven demand without triggering fixed labor cost increases. By treating AI agents as a variable-cost operational layer, banks preserve margin integrity during volume fluctuations while maintaining consistent underwriting standards. This economic model transforms AI from a speculative IT investment into a predictable, revenue-generating workforce asset Top-Rated AI Agents for Financial Services.

Cross-Functional Scalability: Bridging Lending and Adjacent Verticals

The true enterprise value of AI underwriting emerges when the underlying architecture extends beyond lending into adjacent financial verticals. Institutions that successfully deploy AI agents can rapidly repurpose the same decisioning frameworks for insurance operations, including automated policy issuance and claims processing. Both domains rely on identical core competencies: data ingestion, risk scoring, compliance validation, and exception routing. By standardizing automation protocols across lending and insurance, enterprises eliminate redundant development cycles and achieve exponential operational efficiency.

A unified digital workforce architecture enables underwriting logic, fraud detection modules, and regulatory compliance engines to operate interchangeably across product lines. When a commercial borrower simultaneously purchases property or liability coverage, a shared AI agent synchronizes risk assessments, eliminates duplicate documentation requests, and generates consolidated pricing models. This cross-functional integration elevates the customer experience while drastically reducing internal administrative overhead.

Scaling a performance-driven workforce across multi-product portfolios requires centralized governance and interoperable data pipelines. Rather than isolating AI tools by department, institutions should establish enterprise-wide performance benchmarks that measure total cost displacement, processing velocity, and portfolio risk reduction. As insurance automation agents and lending underwriters share training data and compliance frameworks, model accuracy compounds across the organization. The result is a cohesive, scalable AI ecosystem that drives measurable ROI across the entire financial services balance sheet, positioning institutions for sustained operational dominance.

Conclusion

The era of experimental AI pilots has ended. Financial institutions that will lead the next decade treat loan underwriting automation as a disciplined, outcome-driven workforce deployment. By integrating secure API architectures, embedding regulatory compliance, and adopting pay-for-performance contracting, banks can systematically replace overhead with verifiable ROI. At Meo, we engineer AI agents that deliver measurable results, scale elastically, and operate with full accountability. If your institution is prepared to transition from speculative software procurement to performance-driven workforce expansion, contact Meo to implement a risk-aware, results-guaranteed AI underwriting framework tailored to your lending portfolio.